The outlook for the semiconductor market for the remainder of 2015 is mixed. Intel’s 3Q 2015 revenues were up 10% from 2Q 2015 and guidance is for 2.3% growth in 4Q 2015. Most other companies which have announced 3Q 2015 results expect revenue declines in 4Q 2015. The most severe drops (based on the midpoint of company guidance) are -16% from NXP and -13% Freescale. NXP is in the process of acquiring Freescale, with the deal expected to close by the end of the year. Some of the weakness in the NXP and Freescale 4Q 2015 outlooks may be due to customers being cautious and waiting to see how the acquisition works out.

Key Semiconductor Company Revenue |

||

Change versus prior quarter in local currency |

||

|

|

Reported |

Guidance |

Company |

3Q15 |

4Q15 |

Intel |

10% |

2.3% |

Samsung |

14% |

n/a |

SK Hynix |

6.2% |

n/a |

Micron Technology |

-6.6% |

-3.5% |

Texas Instruments |

6.1% |

-6.7% |

STMicroelectronics |

-1.0% |

-6.0% |

NXP |

1.1% |

-16% |

Freescale |

-6.5% |

-13% |

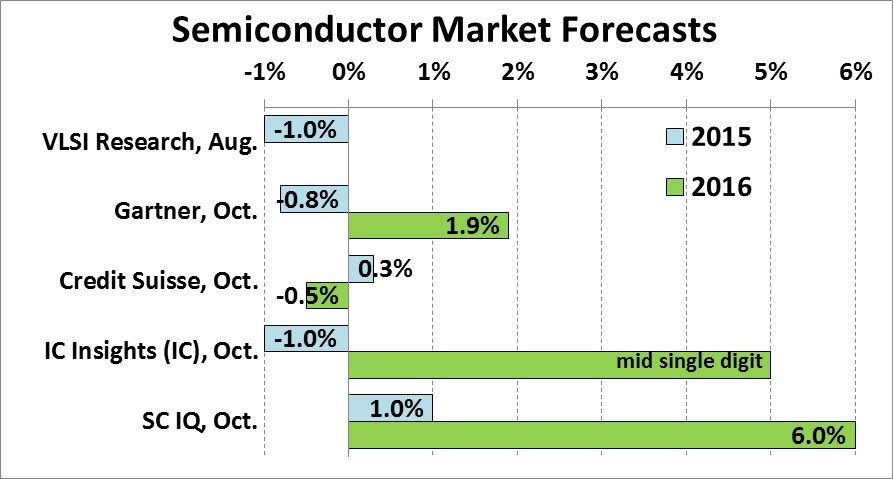

The latest forecasts for 2015 semiconductor market growth range from a 1% decline (VLSI Research and IC Insights) to 1% growth (our latest forecast at Semiconductor Intelligence). The outlook for 2016 ranges from a negative 0.5% from financial services company Credit Suisse to a positive 6.0% from Semiconductor Intelligence (SC IQ).

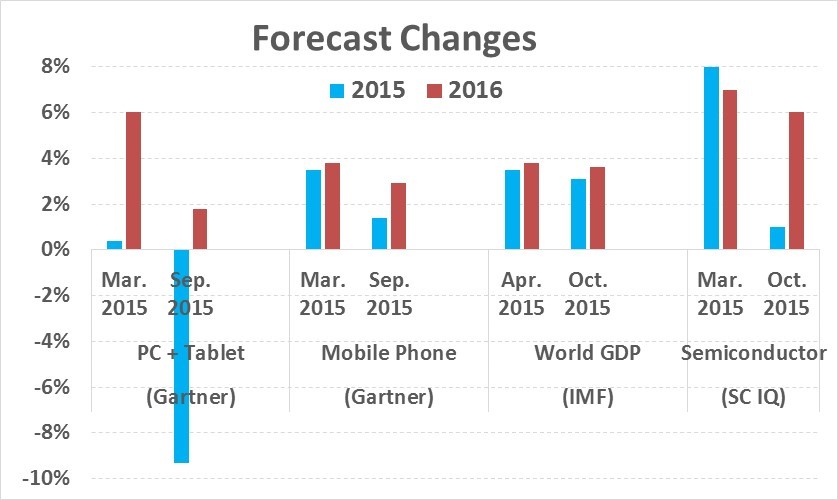

Earlier in 2015 analysts were more optimistic with several forecasts for semiconductor growth of 7% or higher. Our March 2015 forecast at Semiconductor Intelligence was 8%. As the year developed, it became apparent the global economy and electronics end markets were weaker than expected. The chart below compares forecasts for 2015 and 2016 from Gartner released in March 2015 and September 2015 for PCs + tablets and for mobile phones. The most significant change was 2015 PC + tablet shipments dropping from 0.4% growth in March to a 9.3% decline in September. The 2015 mobile phone forecast dropped from 3.5% in March to 1.4% in September. 2016 forecasts changed less, with PCs + tablets dropping from 6% to 1.8% and mobile phones dropping from 3.8% to 2.9%.

The 2015 global GDP forecast from the International Monetary Fund (IMF) also dropped in the last six months from 3.5% in April to 3.1% in October. The 2016 forecast dropped moderately, from 3.8% to 3.6%. Our semiconductor market forecast at Semiconductor Intelligence went from 2015 growth of 8% in March to 1% in September. Our 2016 forecast has decreased only slightly, from 7% in March to 6% in October.

Why is the change in 2016 forecasts not as significant as the change in 2015 forecasts? A skeptic might say analysts do not alter their forecasts until actual data begins to prove them wrong. We are not quite that cynical. The IMF forecast for 2015 dropped from 3.5% to 3.1% primarily due to slower than expected growth in the U.S., a deeper than expected downturn in South America, slower growth in the Middle East because of falling oil prices, and growth slightly below expectations in India and Southeast Asia. Despite all the concern in the media about slowing growth in China, the IMF’s October forecast for 6.8% growth in 2015 and 6.3% growth in 2016 are unchanged from the April forecast. Conditions still point to GDP growth acceleration in 2016. Despite slower growth in China, the advanced economies (including the U.S., Europe and Japan) should improve in 2016. Russia and South America are expected to begin to recover from 2015 recessions. India and Southeast Asia GDP growth should accelerate in 2016.

We at Semiconductor Intelligence feel confident about reasonable growth in the semiconductor market in 2016. Although there are some areas of concern in the global economy, signs point to better conditions in 2016. The key end markets for semiconductors (PCs, tablets and mobile phones) are also expected to improve in 2016.