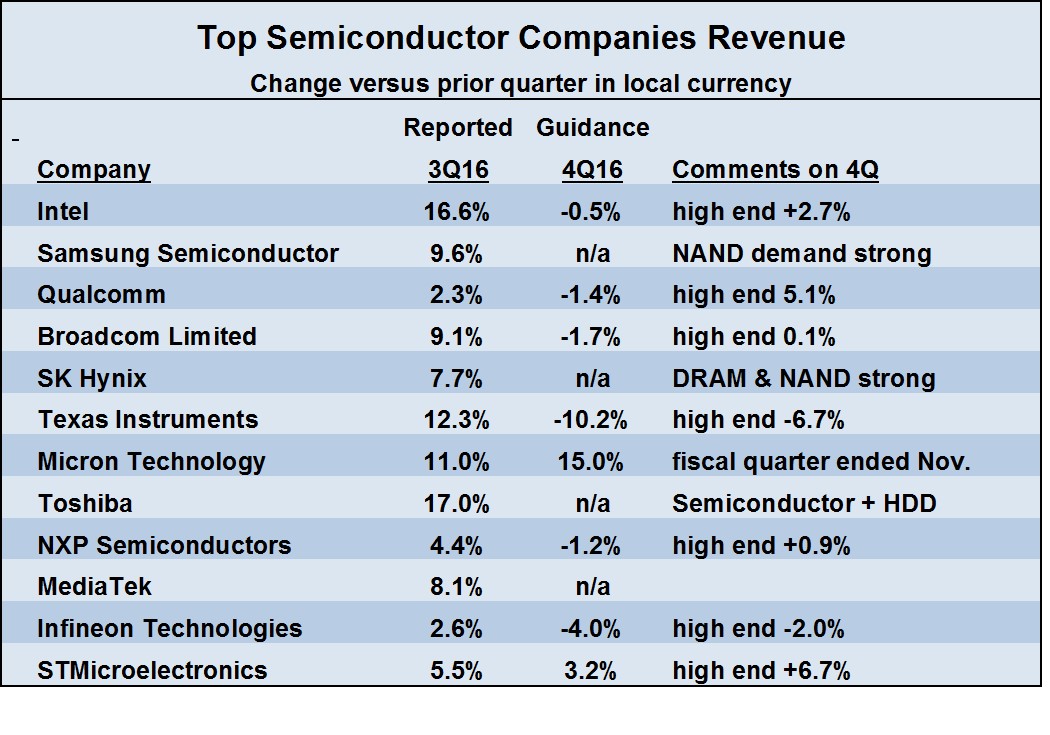

The global semiconductor market posted strong 11.6% growth in 3rd quarter 2016 from 2nd quarter, according to WSTS. This strength is reflected in the 3rd quarter revenue growth reported by the major semiconductor suppliers. Of the 12 companies, half (Intel, Samsung, Broadcom, TI, Micron and Toshiba) reported growth of over 9%. The other six companies reported revenue growth in range of 2.3% to 8.1%.

The 4th quarter of 2016 looks weak based on the available guidance from the above companies. Six companies projected declines in 4th quarter revenue from 3rd quarter based on the midpoint of their guidance. But the upper end of guidance from four of these companies (Intel, Qualcomm, Broadcom and NXP) is for 4th quarter growth. Only Micron Technology (for its fiscal quarter ended in early December) and STMicroelectronics are guiding for increases based on midpoint guidance. Samsung and SK Hynix did not provide revenue guidance, but both stated demand for their memory products will be strong in the 4th quarter.

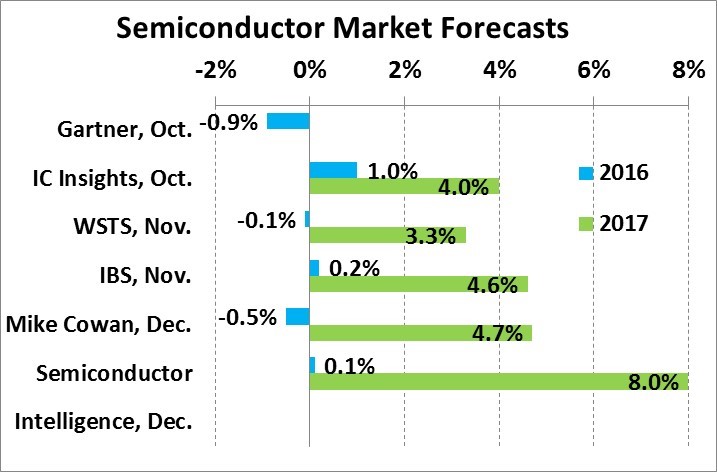

2016 will be another basically flat year for the semiconductor market following a 0.2% decline in 2015. Recent forecasts call for a range of a 0.9% decline (Gartner) to a 1% increase (IC Insights). Our Semiconductor Intelligence projection in August was a 2% decline. However with the strong 11.6% 3rd quarter growth, a modest 1.3% gain in 4th quarter would drive a slight 0.1% annual growth in 2016. We are confident overall 4th quarter market growth will be sufficient to drive a slight positive gain for the semiconductor market in 2016. We are revising our 2016 forecast to 0.1% growth.

The projections for 2017 are generally for moderate growth in the semiconductor market, with most in the 3% to 5% range. Our latest forecast at Semiconductor Intelligence is 8% growth in 2017, the same as in our August forecast. The scenario is based a moderate improvement in end demand for electronics, the quarterly trend driven by 2016 and a modest inventory recovery. In October, Gartner projected the total units of PCs plus tablets would decline 0.7% in 2017 after an 8.7% decline in 2016. Total mobile phones should move from a 1.6% decline in 2016 to a 1.2% increase in 2016. IC Insights in November called for a slight acceleration in smartphone unit growth from 4% in 2016 to 5% in 2017. Thus no strong growth in key electronics devices in 2017, but an improvement from 2016.

Annual change |

2016 |

2017 |

Source |

PC + tablet units |

-8.7% |

-0.7% |

Gartner, Oct. 2016 |

Mobile phone units |

-1.6% |

1.2% |

Gartner, Oct. 2016 |

Smartphone units |

4% |

5% |

IC Insights, Nov. 2016 |

World GDP |

3.1% |

3.4% |

IMF, Oct. 2016. |

The world economy should show modest improvement in 2017, with GDP growing 3.4% compared to 3.1% in 2016 according to the International Monetary Fund (IMF). Among advanced economies, improved GDP growth from the U.S., Canada and Japan will more than offset weaker growth in the UK and Euro Area countries. In emerging and developing economies, steady growth in India and southeast Asia and recoveries in Russia and Latin America should more than compensate for slowing China growth.

Downside risks to the forecast are significant. The impact of Brexit, the UK’s vote to withdraw from the European Union, is difficult to estimate. U.S. President-elect Donald Trump has threatened high tariffs against China. A trade war between China, the largest electronics producer, and the U.S., the second largest electronics consumer after China, would negatively impact the electronics and semiconductor markets in the near term. The continuing conflicts in the Middle East and global terrorism threats could also disrupt the economy. Despite these risks, the overall global economy is healthy and should show modest improvement in 2017.