U.S. President Biden announced on Wednesday an agreement to provide Intel with $8.5 billion in direct funding and $11 billion in loans under the CHIPS and Science Act. Intel will use the funding for wafer fabs in Arizona, Ohio, New Mexico, and Oregon. As reported in our December 2023 newsletter, the CHIPS Act provides a total of $52.7 billion for the U.S. semiconductor industry, including $39 billion in manufacturing incentives. Prior to the Intel grant, the CHIPS Act had announced grants totaling $1.7 billion to GlobalFoundries, Microchip Technology, and BAE Systems, according to the Semiconductor Industry Association (SIA).

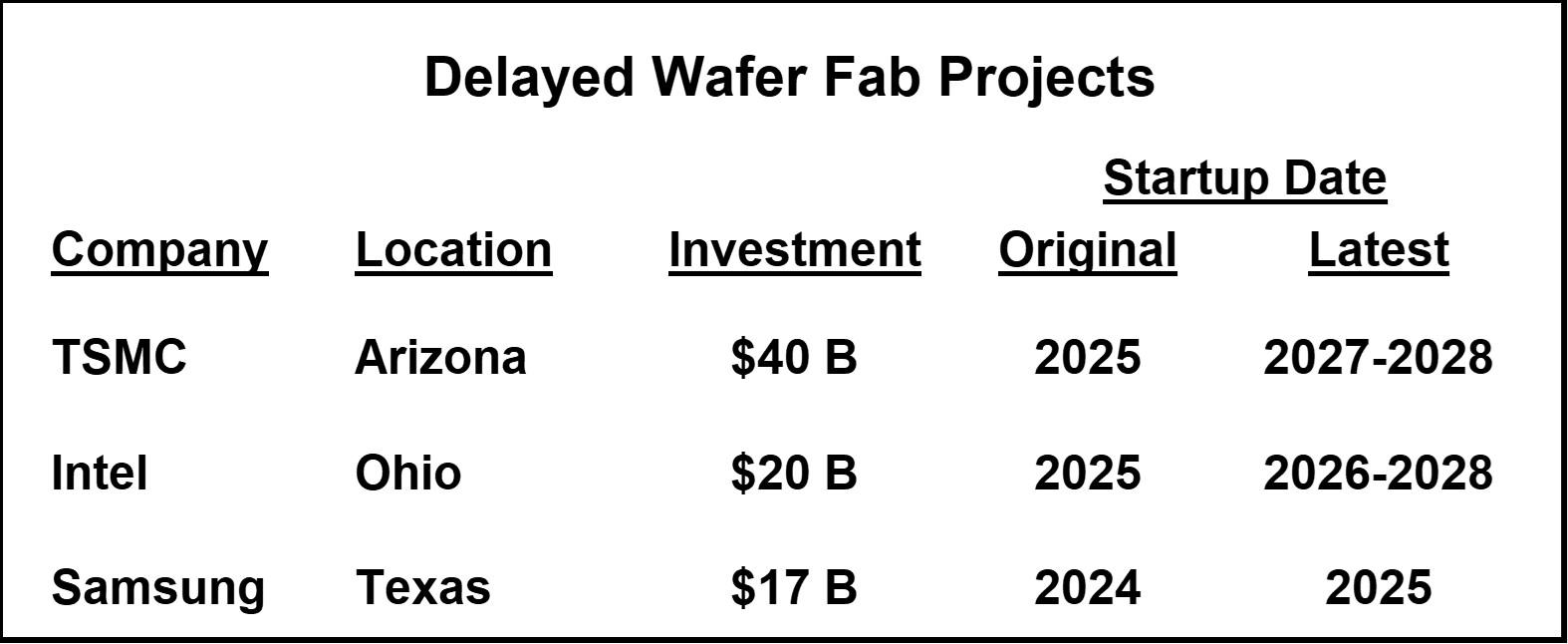

Grants under the CHIPS Act have been slow in coming, with the first grants announced over a year after passage. Some major fab projects in the U.S. have been delayed due the slow disbursement. TSMC also cited difficulties in finding qualified construction personnel. Intel said the delay was also due to slowing sales.

Other nations have also allocated funds to promote semiconductor production. The European Union in September 2023 passed the European Chips Act which provides for 43 billion euro (US$47 billion) of public and private investment in the semiconductor industry. In November 2023, Japan allocated 2 trillion yen (US$13 billion) for semiconductor manufacturing. Taiwan in January 2024 enacted a law to provide tax breaks for semiconductor companies. South Korea in March 2023 passed a bill to provide tax breaks to strategic technologies including semiconductors. China is expected to create a $40 billion fund backed by the government to subsidize its semiconductor industry.

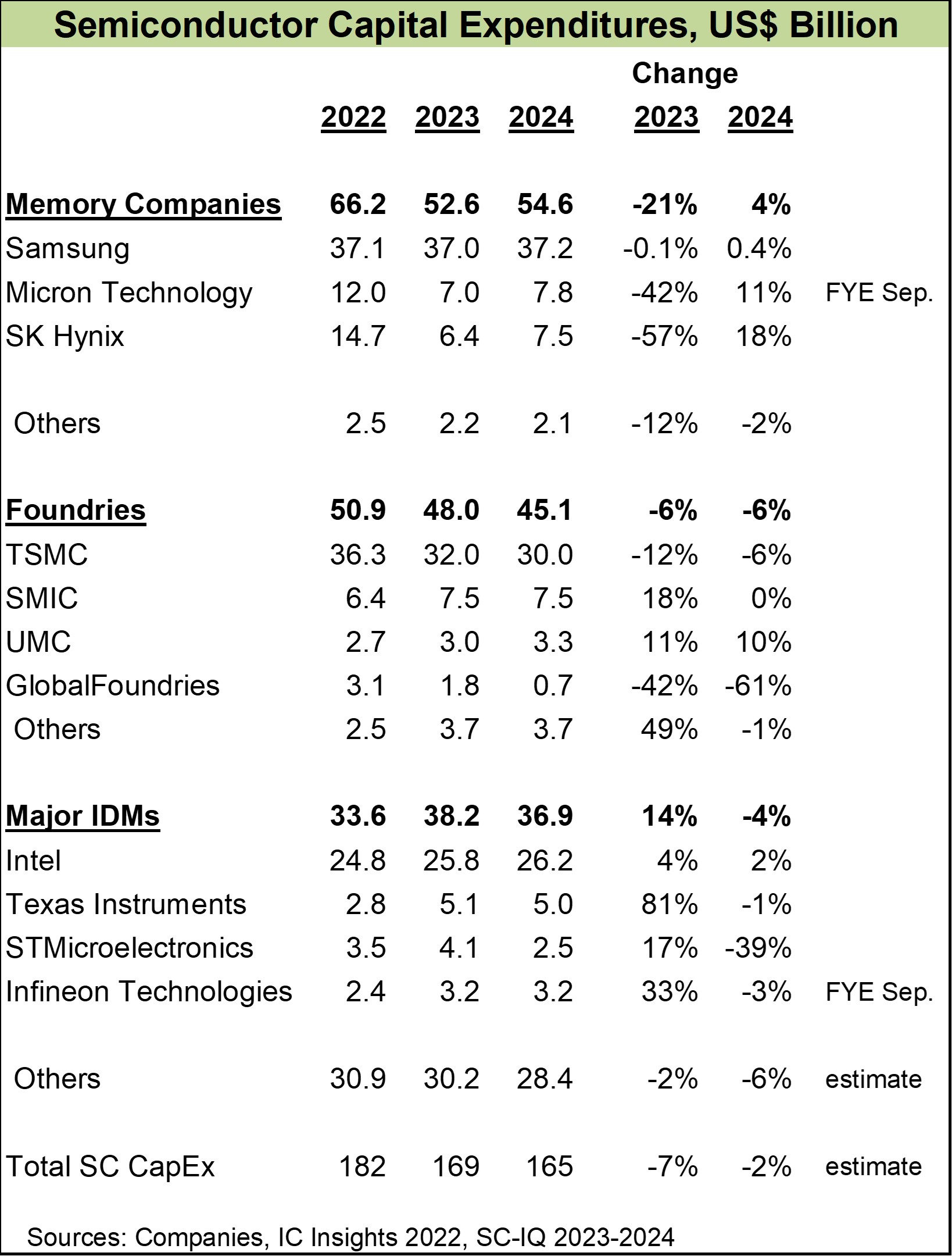

What is the outlook for capital expenditures (CapEx) in the semiconductor industry this year? The CHIPS Act was designed to spur CapEx, but much of the effect will not occur until after 2024. After a disappointing 8.2% decline in the semiconductor market last year, many companies are cautious about CapEx in 2024. We at Semiconductor Intelligence estimate total semiconductor CapEx in 2023 was $169 billion, down 7% from 2022. Our forecast is a 2% decline in CapEx in 2024.

The major memory companies are generally increasing CapEx in 2024 as the memory market recovers and new applications such as AI are expected to increase demand. Samsung plans relatively flat spending in 2024 at $37 billion but did not cut CapEx in 2023. Micron Technology and SK Hynix cut back CapEx significantly in 2023 and are planning double-digit increases in 2024.

The largest foundry, TSMC, plans to spend about $28 billion to $32 billion in 2024, with the midrange of $30 billion down 6% from 2023. SMIC is planning flat CapEx while UMC plans a 10% increase. GlobalFoundries expects a 61% cut in 2024 CapEx but will ramp up spending in the next few years as it builds a new fab in Malta, New York.

Among integrated device manufacturers (IDMs), Intel plans to increase CapEx in 2024 by 2% to $26.2 billion. Intel will increase capacity for foundry customers as well as for internal products. Texas Instruments’ CapEx is roughly flat. TI plans to spend about $5 billion a year through 2026, primarily for its new fabs in Sherman, Texas. STMicroelectronics will cut CapEx 39% while Infineon Technologies will cut by 3%.

The three largest spenders – Samsung, TSMC and Intel – will account for 57% of semiconductor industry CapEx in 2024.

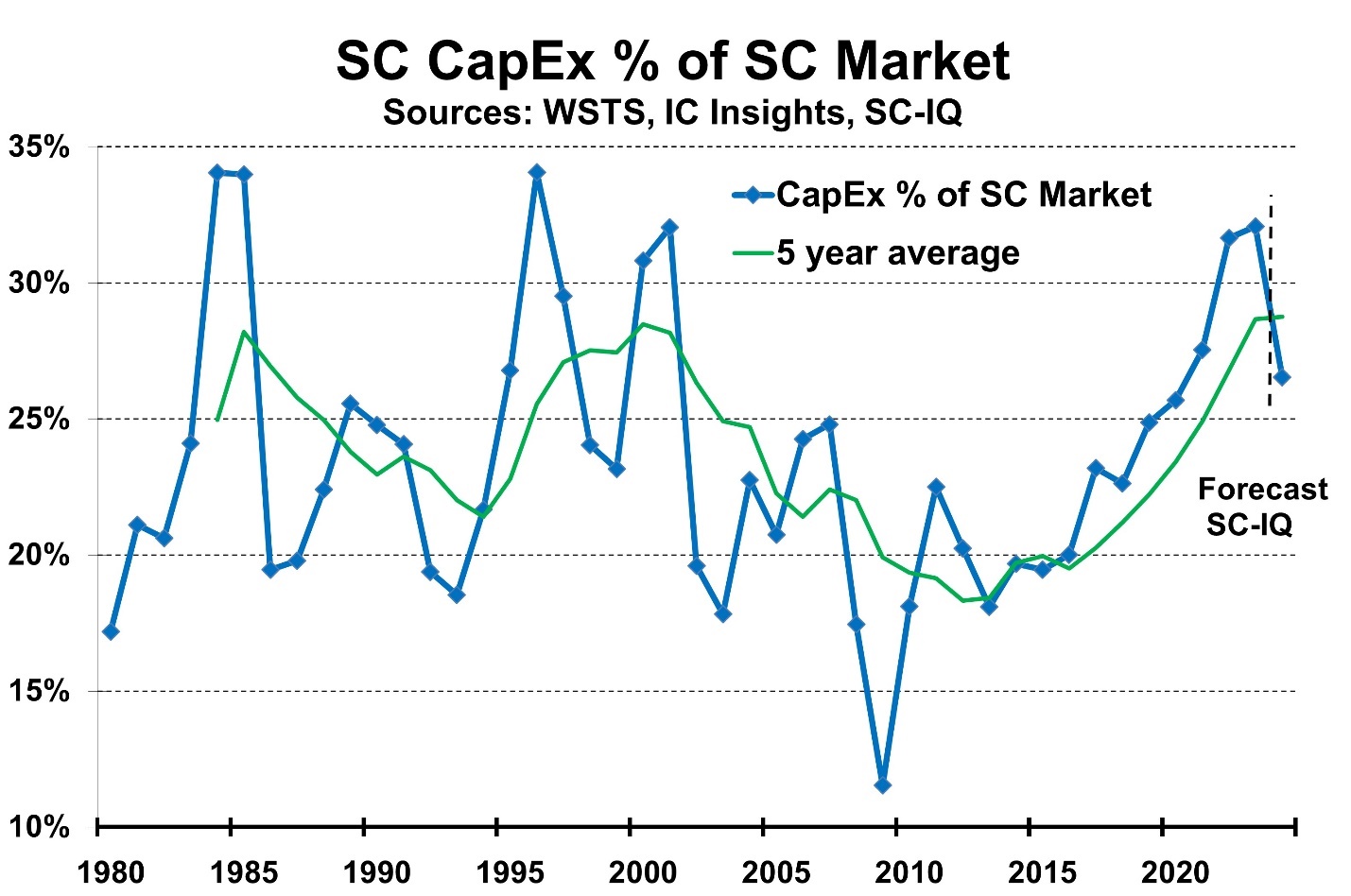

What is the appropriate level of CapEx relative to the semiconductor market? The semiconductor market is notoriously volatile. Over the last 40 years, annual change has ranged from 46% growth in 1984 to a 32% decline in 2001. Although the industry has become somewhat less volatile as it has matured, in the last five years it has shown a 26% increase in 2021 and a 12% decrease in 2019. Semiconductor companies need to plan their capacity several years out. It takes about two years to build a new wafer fab and additional time for planning and financing. As a result, the ratio of semiconductor CapEx to the semiconductor market varies greatly, as shown below.

The semiconductor CapEx to market size ratio has varied from a high of 34% to a low of 12%. The five-year average ratio ranges between 28% and 18%. Over the total period of 1980 to 2023, the total CapEx was 23% of the semiconductor market. Despite the volatility, the long-term trend of the ratio has been fairly consistent. Based on expected strong market growth and a drop in CapEx, we expect the ratio to drop from 32% in 2023 to 27% in 2024.

Most forecasts for semiconductor market growth in 2024 are in the range of 13% to 20%. Our Semiconductor Intelligence forecast is 18%. If 2024 turns out to be as strong as expected, companies will likely increase their CapEx plans as the year progresses. We could then see positive change in semiconductor CapEx in 2024.