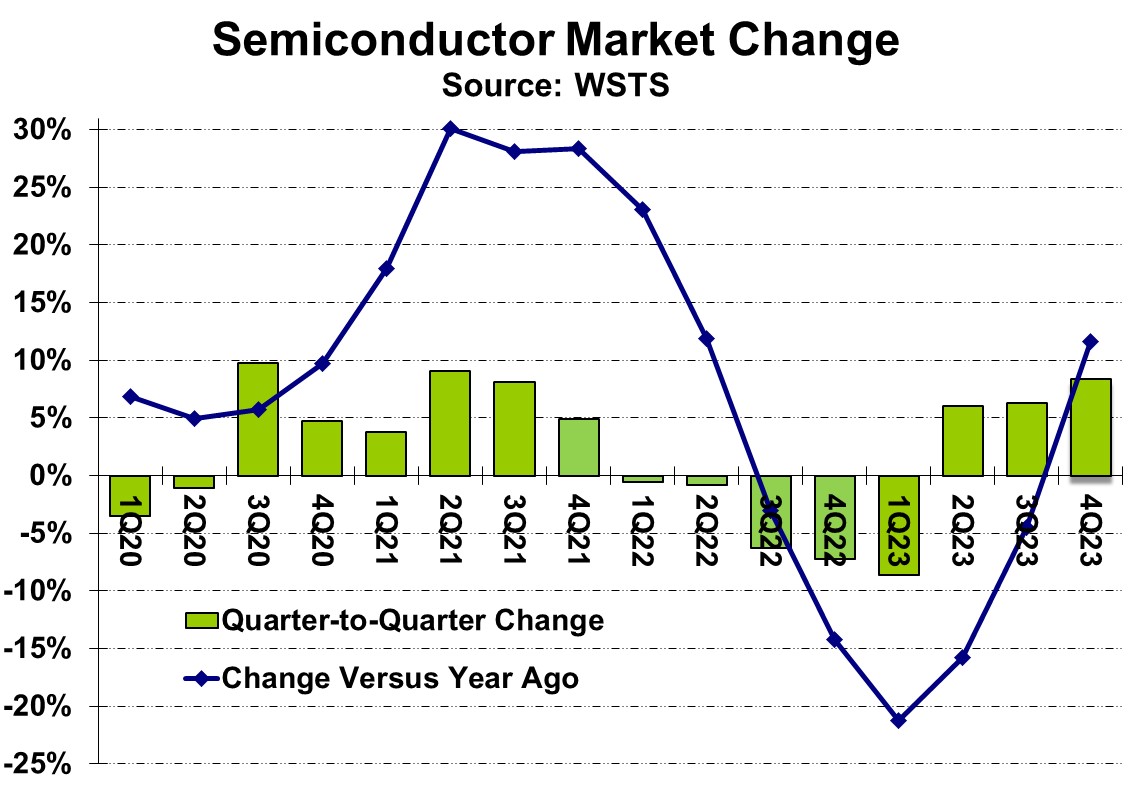

The global semiconductor market grew 8.4% in 4Q 2023 from 3Q 2023, according to WSTS. The 8.4% gain was the highest quarter-to-quarter growth since 9.1% in 2Q 2021. This was also the highest 3Q to 4Q increase in 20 years, since an 11% rise in 4Q 2003. 4Q 2023 was up 11.6% from a year ago, following five quarters of negative year-to-year change.

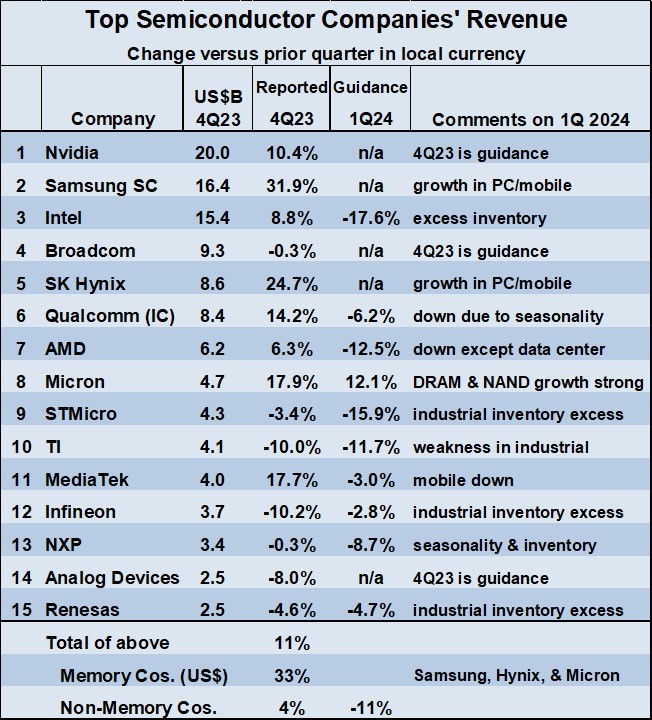

The robust 4Q 2023 gain was primarily driven by memory. The major memory companies all reported healthy revenue growth in 4Q 2023 from 3Q 2023. In U.S. dollars, Samsung’s memory business was up 49%, SK Hynix was up 24.1%, and Micron Technology was up 17.9%. The weighted-average revenue growth in U.S. dollars of these three businesses was 33%. The weighted-average revenue growth of the twelve largest non-memory companies was 4% in 4Q 2023 from 3Q 2023. The highest increases of the non-memory companies were 17.7% from MediaTek, 14.2% from Qualcomm, and 10.4% from Nvidia. Seven of these non-memory companies had decreased 4Q 2023 revenue, with the largest declines being 10.2% from Infineon Technologies, 10.0% from Texas Instruments, and 8.0% from Analog Devices.

The outlook for 1Q 2024 revenue change from 4Q 2023 is mostly negative, except for the memory companies. Micron expects 12.1% growth. Samsung and SK Hynix did not provide specific guidance, but both indicated continuing strong memory demand. The nine non-memory companies providing revenue guidance projected 1Q 2024 declines ranging from 2.8% from Infineon to 17.6% from Intel. The expected decreases were blamed on seasonality, excess inventories, and weakness in the industrial sector.

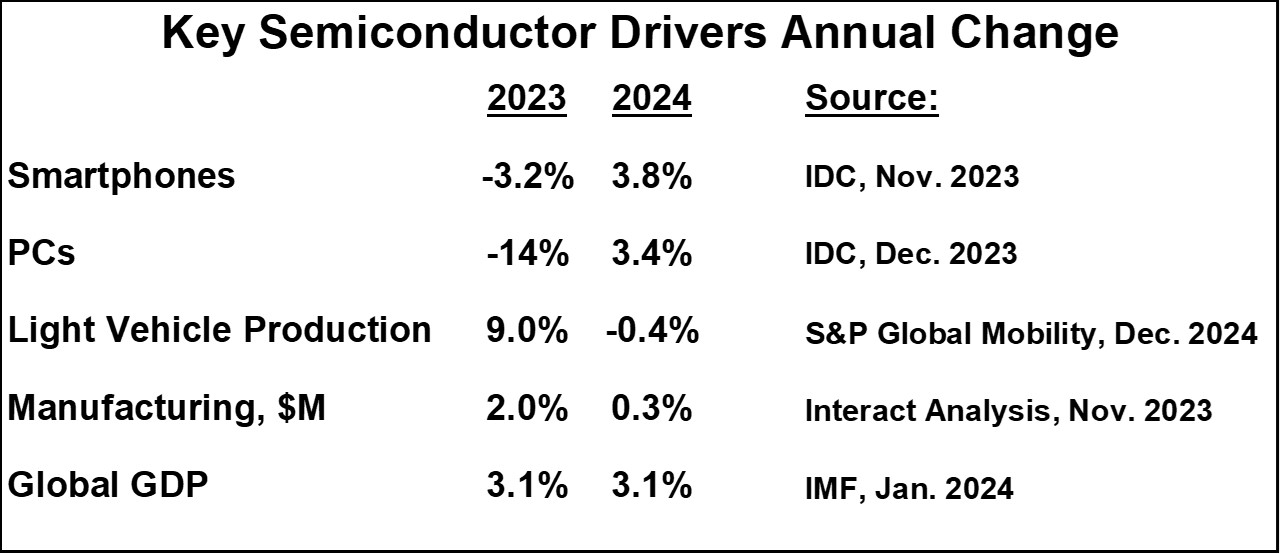

The 2024 projections for key drivers of the semiconductor market help explain the divergent projections. Smartphone unit shipments were down 3.2% in 2023 but IDC expects them to rebound to a 3.8% increase in 2024. Smartphones drive revenue growth for the memory companies and for Qualcomm and MediaTek. PC unit shipments dropped a dramatic 14% in 2023. IDC projects PC growth of 3.4% in 2024. The PC rebound benefits the memory companies and the processor companies (Intel, Nvidia, and AMD).

The automotive and industrial markets have been major revenue drivers for several companies as other end markets have been weak. However, automotive production increases appear to be ending in 2024. S&P Global Mobility forecasts a 0.4% decline in production of light vehicles in 2024 following strong 9% growth in 2023. S&P says vehicle production and inventory restocking have satisfied post-pandemic demand and now exceed current customer demand. Global manufacturing (industrial production) is expected to moderate from 2.0% growth in 2023 to 0.3% growth in 2024 according to Interact Analysis. This indicates slower demand from the industrial sector. The slowdown in the automotive and industrial sectors primarily impacts STMicroelectronics, Texas Instruments, Infineon Technologies, NXP Semiconductors, Analog Devices and Renesas Electronics.

Global GDP is projected to rise 3.1% in 2024, the same as in 2023, according to the International Monetary Fund (IMF). Thus, the overall economy is not expected to show any significant acceleration or deceleration. However, some countries are showing weakness. The United Kingdom slipped into a recession with contracting GDP in the last two quarters of 2023. Japan also entered a recession after two quarters of GDP declines.

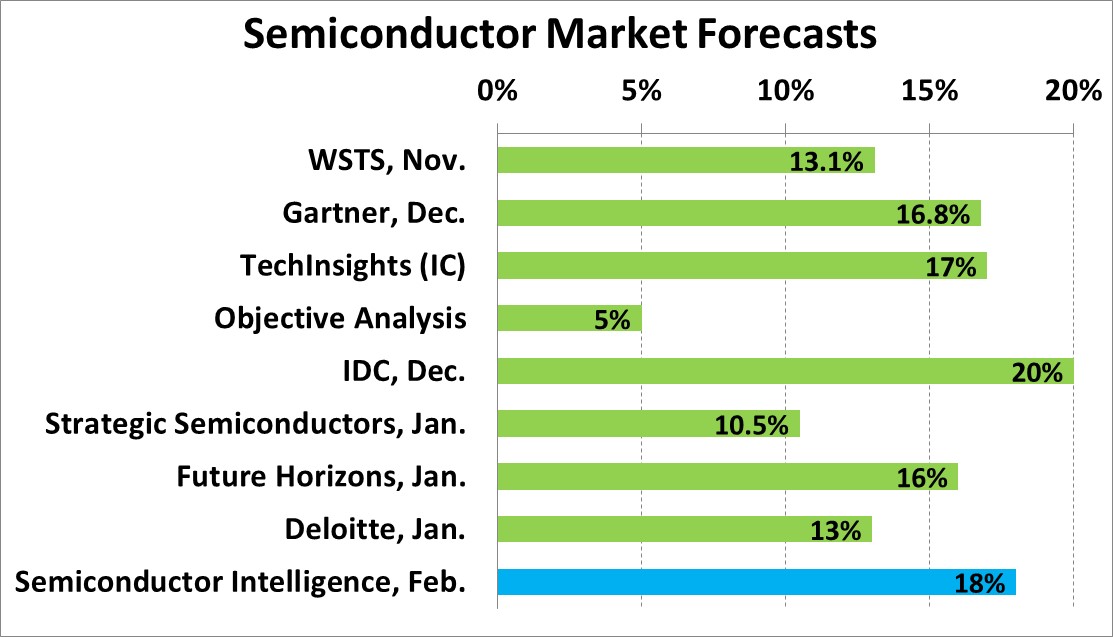

Gains in the 2024 semiconductor market will be driven by memory. WSTS forecast 44.8% growth for memory and 6.5% growth for non-memory, resulting in total market growth of 13.1% in 2024. Gartner assumed a 66% increase in memory in its forecast of a 16.8% increase in the total market. Memory will be driven by recoveries in the PC and smartphone markets. These two sectors will also aid the non-memory market, but other non-memory market drivers such as automotive and industrial will be weaker in 2024.

Against this backdrop, what is the outlook for the overall semiconductor market in 2024? Most forecasters expect robust growth, with IDC the highest at “above 20%.” Objective Analysis projects “below 5%” growth as they expect the memory boom will not be sustainable. Our latest forecast from Semiconductor Intelligence is an 18% increase. Other projections range from 10.5% to 17%.

Forecast contest winner

The final WSTS data for 2023 showed the semiconductor market declined 8.2% for the year. Going into 2023, the semiconductor market was certain to decline after each quarter of 2022 showed a quarter-to-quarter decline. Each year we at Semiconductor Intelligence award a virtual prize for the most accurate forecast made from November of the prior year through February of the forecast year (before the first WSTS data for January is released). 2023 forecasts released in November 2022 through February 2023 ranged from minus 3.6% to minus 22%. The winner for 2023 is Bill McClean of IC Insights (now part of TechInsights) with a forecast of minus 6%. Congratulations to Bill who retired at the end of 2022 after 42 years of following the semiconductor Industry.